3/2026 Uncertainty is Certain

Welcome to the March edition of my Market Newsletter. I keep finding there’s an abundance of noise and confusion in the financial markets, and most Americans don’t know how to cut through the noise and get the data they are really looking for to make informed decisions. Because of this, I’ve created this newsletter, where each month I put together a summary of thinking’s to help educate long-term decisions. With that said, let’s get to it!

Disclaimer: Because of the increased regulation and compliance in the financial industry, I want to start with saying everything in this newsletter is based on my opinion, is not predictive in any way, and in an effort to make this content as accessible as possible, AI was used to help re-write my content and remove grammatical errors.

Full written article below with sources.

If you’ve turned on the news recently, you have likely felt a familiar tightening in your chest. Between the escalating conflict in Iran and the lingering aftershocks of last year’s “Tariff Typhoon,” it feels as though we are living through a period of uniquely high uncertainty. The headlines suggest that the world is more volatile than ever, and the temptation to "do something" to protect your hard-earned capital is reaching a fever pitch.

Because of this, I want to remind everyone: Uncertainty in the investing markets is not a temporary bug in the system; it is a permanent feature of successful investing.

Let me explain.

The term "principled consistency" isn't just a tagline; it's a recognition that while we can’t control the world, we can control our reaction to it. To help navigate these headlines, I’ve distilled a framework for some information, followed by a deeper look at how history and risk actually function.

Wisdom for the Fog: Core Themes for the Current Moment

Drawing from recent market insights and Ben Carlson’s "10 Rules for Dealing with Uncertainty," we can condense the path forward into four essential themes: aWealthOfCommonSense.com

Focus on the "Controllables": You cannot control the Fed, the Iranian military, or global trade policy. However, you have total control over your savings rate, your asset allocation, and, most importantly, your behavior. In an uncertain world, your behavior is your greatest asset or your greatest liability.

Discipline Over Optimization: You don’t need a complex or "perfect" portfolio to reach your goals; you need a plan you can actually stick with when things get uncomfortable. The most sophisticated answer is often the simplest plan.

The Nature of Risk: True risk is rarely the headline everyone is already talking about (which the market has likely already priced in). Real risk is the "unknown unknowns" that no one sees coming. Because the future is inherently unpredictable, "doing nothing" can often be a an informed, disciplined decision.

Maintain Constructive Skepticism: It is healthy to be skeptical of sensational predictions. However, avoid cynicism. Cynicism leads you to believe that progress has stopped - a bet that has been wrong for centuries.

Why “This Time” is Never Different

We tend to view historical investing like a smooth, inevitable upward line. In contrast, we view the present with all present data available. An overload of data, most of which is from companies that are paid to get “clicks” – which most seem to be negative headlines because that creates the most financial incentive. In reality, and historically, every period of significant growth was punctuated by "existential" crises that felt just as dire then as our current headlines do today.

Consider the context of 1973. When the Arab oil embargo caused prices to quadruple and the Watergate scandal paralyzed the government, people didn't think, "This is a great buying opportunity." They thought the American experiment was over. When the dot-com bubble burst in 2000, followed by the trauma of 9/11, the prevailing wisdom was that "buy and hold" was dead. During the 2008 financial collapse, the fear wasn't just a market drop; it was the total disintegration of the global banking system.

Yet, despite these "existential" threats, shareholder capitalism remained intact.

Why?

Because great companies do not sit idly by during a crisis. They do what any rational person would do. They cut costs, they innovate, they acquire weaker competitors, and they find ways to provide value in a changing world.

The math of resilience is staggering: A $100,000 investment in the S&P 500 in January 1973, at the very start of a decade of stagflation, oil shocks, and political crisis, would have grown to over $24.7 million by the end of 2025 (source). That is a compound annual growth rate of 10.9% through 53 years of uncertainty.

History proves that the global economy advances. When you step back and think about this, it seems that innovation is birthed from the chaos.

Redefining Your Greatest Risk: Volatility vs. Erosion

As your advisor, one of my most important jobs is to help you distinguish between "market noise" and "actual risk." I find it’s very common to mistake volatility for risk.

Volatility is the temporary decline in your account balance during a market correction, like the 21% drop we saw during the Tariff Typhoon of 2025. Volatility is uncomfortable, but it is not a loss unless you sell. It is simply what some call the "price of admission" the market charges for long-term returns.

The Real Risk…the one we should actually fear…is the permanent erosion of your purchasing power. This is the risk that your money loses its ability to buy the goods and services you need to live a dignified life. This is simply understood as keeping up with and excelling past inflation in an after-tax manner.

The Trap of "Safety": When headlines get scary, most have the instinct to flee to the "safety" of cash or bonds. But over the last 50 years, cash has been one of the most dangerous place for a long-term investor. Cash history has not kept up with inflation, which in turn creates a loss of purchasing power.

Compounding Income: Consider the growth of dividends. In 1996, 30 years ago, the cash dividend of the S&P 500 was $13.89; by Feb 2026, it had risen to $79.94 - an increase of over 420%. During that same period, consumer prices only roughly doubled. You didn’t ask, but I’ll share it anyway, if you invested the same 100k in 1996, you’d now have over 1.9mil.

When you own a diversified portfolio of global equities, you aren't just "betting on stocks." You are owning a share of companies that are transparent, audited, and motivated to make money for you, the shareholder. These companies have a history of raising their share prices and growing their earnings faster than inflation, protecting your family’s standard of living in a way that "safe" assets never can.

My goal is for you to work towards peace of mind, not because the world is certain, but because your plan is built to withstand uncertainty. Money is a tool, something to be acted upon to accomplish your goals for your family.

I don’t pretend to have a secret formula or a crystal ball that can predict the outcome in Iran or the next market swing. What I do have is a process designed to create consistent, personal outcomes by adhering to the principles that have worked for over a century.

If the current environment has you feeling anxious about your "Financial Blueprint," let's schedule a time to talk. We will share the truth kindly, look at the data, and ensure your money is working as hard for your family as you did to earn it.

If you do not feel 100% confident in your plan, I invite you to reach out. I am always available to discuss.

Additional Data: Each month I get asked by clients what additional resources I’m looking at. Please hear me in stating I’m not trying to predict anything whatsoever; this is just some of the interesting data I’m watching.

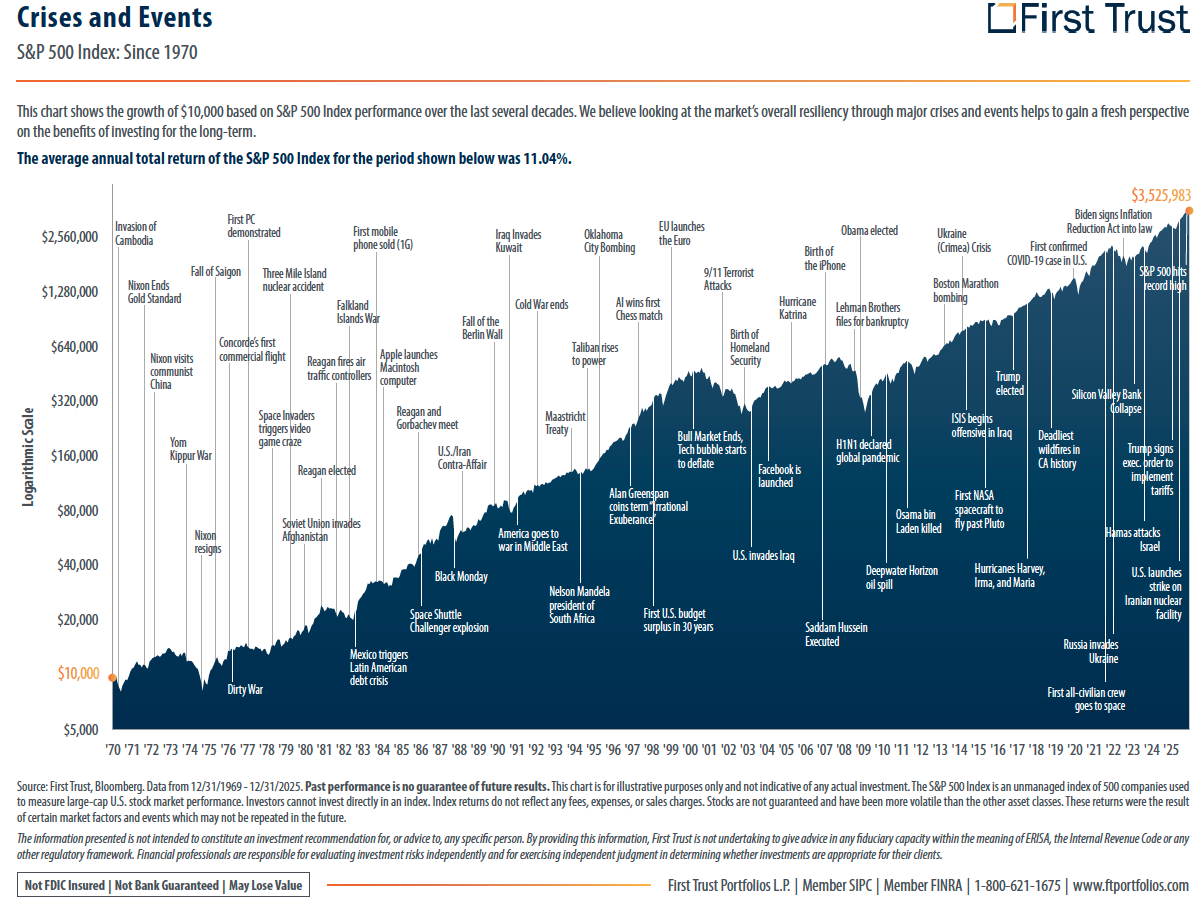

“Why should I own anything other than the S&P 500?” – this has been one of the most common questions from clients… well… here’s a compelling chart…

Make it stand out

Whatever it is, the way you tell your story online can make all the difference.

Yes, I am guilty of looking at chart like this a lot. I find I’m always surprised to see the dramatic moves of the market over the years.

Breakeven Inflation Rate - 5-Year Breakeven inflation rate is now 2.46%. When you study this chart, you’ll see it goes back to 2004. From this past month, the inflation rate has ticked higher.

Debt Interest Payments – Most in this country would agree that the Federal Debt is just too high, but did you realize that the interest payments on this debt is now just under 1.2 trillion a year? What should we do about it? My guess is we should balance the government budget….but no one is asking me. What’s more, there’s about 3 Trillion in debt to be reissued in 2026 and the broad assumption is that the new interest rates will be quite a bit higher on the reissued debt. So what will this mean? It’ll likely mean even a greater amount of debt interest payments.

In closing: We of course cannot control what the market does from here and we cannot predict when the next market downturn will occur. But we can control our behavior to these outside events and continue to stick with our long-term investment strategy.

As always, thank you for your trust. If you have any questions/concerns, please contact me. If you found this useful, please share with someone you care about.

-Dave

David Hobbs, CFP®

Wealth Advisor | Owner

Hobbs Wealth Management

Past performance may not be indicative of future results. Investing in securities involves risks, including the potential for loss of principal. There is no guarantee that any investment plan or strategy will be successful.

Standard & Poor’s 500 (S&P 500) - a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy.

Russell 2000 – The index measures the performance of the small-cap segment of the US equity universe. It is a subset of the Russell 3000 and includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership.

MSCI ACWI ex USA – The index measures the performance of the large and mid-cap segments of the particular regions, excluding USA equity securities, including developed and emerging markets. It is free float-adjusted market-capitalization weighted.

Federal Funds Rate - refers to the target interest rate set by the Federal Open Market Committee (FOMC). This target is the rate at which commercial banks borrow and lend their excess reserves to each other overnight.

This report was prepared by Hobbs Wealth Management, a State registered investment adviser under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Neither the information nor any opinion expressed it so be construed as solicitation to buy or sell a security of personalized investment, tax, or legal advice. For more information please visit: https://adviserinfo.sec.gov/ and search for our firm name.

This newsletter is prepared to provide a degree of insight into the analysis used by Hobbs Wealth Management to make investment decisions. It is not a complete description of all the factors used by Hobbs Wealth Management to make decisions on behalf of clients. The opinions included are not intended to be taken as fact but are Hobbs Wealth Management’s interpretation of the impact of external events on investments.

The information herein was obtained from various sources. Hobbs Wealth Management does not guarantee the accuracy or completeness of information provided by third parties. The information in this report is given as of the date indicated and is believed to be reliable. Hobbs Wealth Management assumes no obligation to update this information, or to advise on further developments relating to it.

This article contains external links directing you to a third-party website. Although we have reviewed the website prior to creating the link, we are not responsible for the content of the site.

An index is an unmanaged portfolio of specific securities, the performance of which is often used as a benchmark in judging the relative performance of certain asset classes. Investors cannot invest directly in an index. An index does not charge management fees or brokerage expenses, and no such fees or expenses were deducted from the performance shown.

The mention of specific securities and sectors illustrates the application of our investment approach only and is not to be considered a recommendation. The specific securities identified and described herein do not represent all of the securities purchased or sold for the portfolio, and it should not be assumed that investment in these securities was or will be profitable. There is no assurance that the securities purchased remain in the portfolio, or that securities sold have not been repurchased. For a complete list of holdings, please contact your portfolio advisor.

Hobbs Wealth Management may discuss and display charts, graphs, formulas, stock and sector picks which are not intended to be used by themselves to determine which securities to buy or sell, or when to buy or sell them. This specific information is limited and should not be used on their own to make investment decisions. This information is offered as educational only.