2/2026 Evolving Markets

Welcome to the February edition of my Market Newsletter. I keep finding there’s an abundance of noise and confusion in the financial markets, and most Americans don’t know how to cut through the noise and get the data they are really looking for to make informed decisions. Because of this, I’ve created this newsletter, where each month I put together a summary of thinking’s to help educate long-term decisions. With that said, let’s get to it!

Disclaimer: Because of the increased regulation and compliance in the financial industry, I want to start with saying everything in this newsletter is based on my opinion, is not predictive in any way, and in an effort to make this content as accessible as possible, AI was used to help re-write my content and remove grammatical errors.

Full written article below with sources.

As we start 2026, the financial headlines are dominated by transition. Whether it is the shifting of the guard at the Federal Reserve or the significant policy changes emanating from the White House, the news never sleeps.

In some recent conversations, a recurring theme has emerged: concern. Specifically, I have heard questions regarding whether our government will have a "policy mistake" - a decision that could create systemic problems that are difficult to reverse. It could be the Federal Debt, international relationship, domestic policy divides, AI job displacement and others. All of these concerns I’ve heard recently are valid and thoughtful. We are living through a period of change, and change inherently brings a degree of uncertainty.

However, if history serves as our guide, it teaches us that while political cycles bring noise and friction, the broad engine of the American economy is remarkably durable. To use an analogy, governments set the rules of the road, but they do not drive the car. The car is driven by millions of individual participants—entrepreneurs, executives, and workers—who are relentlessly focused on solving problems and generating value. Whatever the policy landscape may be, companies will continue to seek out profits, adapt to new regulations, and find ways to march forward.

The Six-Year Retrospective: A Lesson in Market Resiliency

To find evidence of this durability, we only need to look back six years. February 19th, 2020, marked the final peak of the S&P 500 before the world was upended by the COVID-19 pandemic. On that day, the index closed at 3,386.

In the thirty-three days that followed, we witnessed one of the most violent declines in market history, with the index plunging over 34% to a trough of 2,237. At that moment, the narrative was one of total systemic collapse. Yet, look at where we stand today, six years later. As of February 2026, the S&P 500 has climbed to new heights, currently trading near the 6,900-7,000 level.

This recovery was not fueled by luck. It was fueled by the fundamental mechanics of profit-seeking companies. When the world changed, profit-seeking companies did not simply surrender; they innovated. They digitized their operations, streamlined supply chains, and leveraged emerging technologies. These companies sell products and services at a profit, and as owners of these companies, you are the direct beneficiaries of those profits being returned to shareholders through dividends and growth. This consistency of corporate America, to return shareholder value, is the bedrock of long-term growth in the broad markets.

Institutional Shifts: The Warsh Era at the Federal Reserve

As we look toward the remainder of the year, a major institutional shift is on the horizon. President Trump has slated Kevin Warsh to succeed Jerome Powell as Chair of the Federal Reserve when Powell’s term concludes in the coming months.

In my assessment, a Warsh-led Fed could be highly "additive" for the equity markets. Warsh has long been a proponent of a more streamlined central bank, and his likely approach centers on two key pillars that should encourage market growth:

A Pro-Growth Interest Rate Policy: Warsh has historically been critical of the Fed’s tendency to remain "higher for longer" when the data suggests room for easing. There is a strong expectation that his leadership will lean toward lowering interest rates more aggressively to ensure that the cost of capital does not stifle corporate expansion. Lower rates generally increase the present value of future earnings, which is a powerful tailwind for stock valuations. My thought? I hope Warsh highly communicates the planned moves and that the moves continue to be data dependent.

Reducing the Fed’s Footprint: Perhaps more importantly, Warsh is expected to prioritize a reduction in the size of the Federal Reserve’s balance sheet. He has often spoken about the dangers of "mission creep" within the central bank. By reducing the Fed’s intervention in the bond markets and shrinking its overall footprint, he aims to return more influence to the private sector. A smaller, more disciplined Fed reduces the "noise" in the financial system, allowing market participants to price risk more accurately and efficiently.

Stewardship Through the Noise

As a client of Hobbs Wealth, my commitment is not to react to every headline or predict the unpredictable. My role is to help you maintain a steady hand. My process—the Financial Blueprint—was designed specifically to handle the "unknowns" by focusing on what we can control: our behavior, our costs, and our adherence to a principled strategy.

As I state in my firm’s core principles: the global economy has been advancing since the dawn of time. We don't know exactly where the next spark of growth will come from, but we have faith that it will come. Whether the headwinds are political or economic, the companies we own are designed to weather the changes.

If you do not feel 100% confident in your plan, I invite you to reach out. I am always available to discuss.

Additional Data: Each month I get asked by clients what additional resources I’m looking at. Please hear me in stating I’m not trying to predict anything whatsoever; this is just some of the interesting data I’m watching.

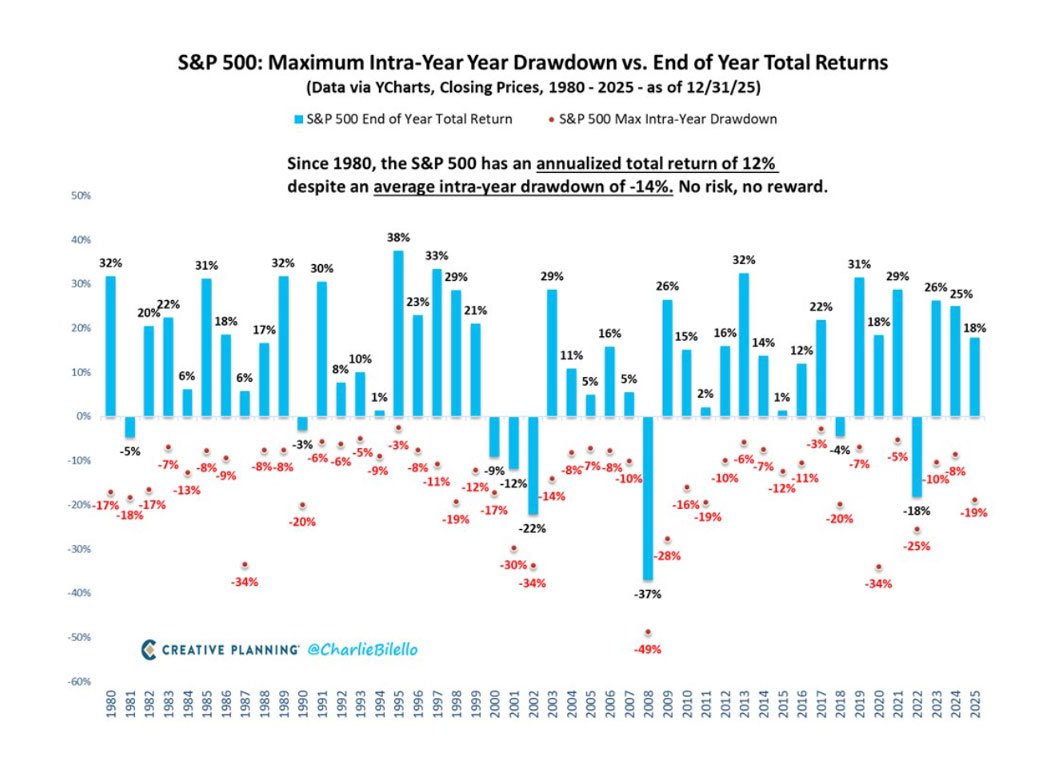

Intra-Year Market Declines – please take you time and review this chart. It’s almost comical how consistent the market downturns are. So what do we do about it? Assume the market will decline double digits at some point this year.

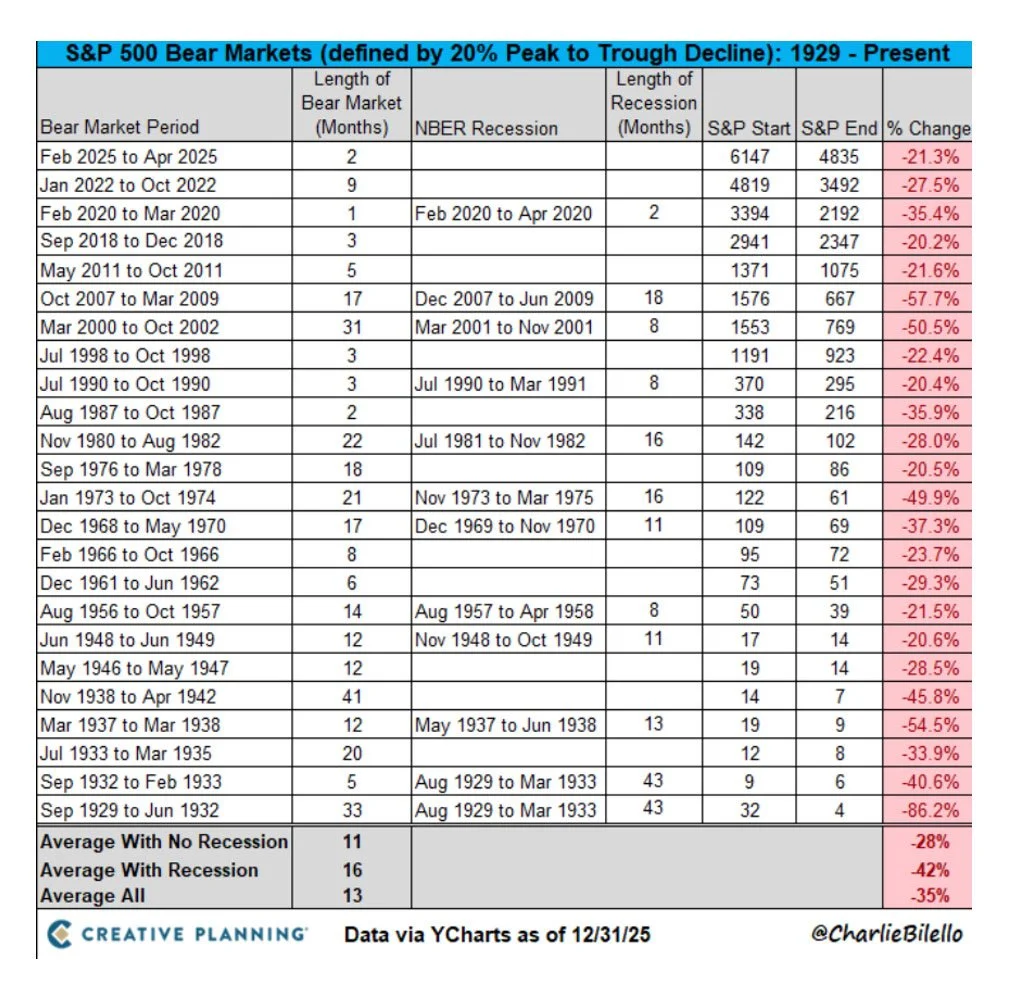

Another chart to study, since the start of the century, there have been 7 occurrences of at least 20% market declines. That’s one about every 3.5 years. What’s more, we had 3 of these occurrences in the past 5 years.

Breakeven Inflation Rate - 5-Year Breakeven inflation rate is now 2.53%. When you study this chart, you’ll see it goes back to 2004. From this past month, the inflation rate has ticked higher.

Debt Interest Payments – Most in this country would agree that the Federal Debt is just too high, but did you realize that the interest payments on this debt is now just under 1.2 trillion a year? What should we do about it? My guess is we should balance the government budget…. But no one is asking me. What’s more, there’s about 3 Trillion in debt to be reissued in 2025 and the broad assumption is that the new interest rates will be quite a bit higher on the reissued debt. So what will this mean? It’ll likely mean even a greater about of debt interest payments.

In closing: We of course cannot control what the market does from here and we cannot predict when the next market downturn will occur. But we can control our behavior to these outside events and continue to stick with our long-term investment strategy.

As always, thank you for your trust, if you have any questions/concerns please contact me. If you found this useful, please share with someone you care about.

-Dave

David Hobbs, CFP®

Wealth Advisor | Owner

Hobbs Wealth Management

Past performance may not be indicative of future results. Investing in securities involves risks, including the potential for loss of principal. There is no guarantee that any investment plan or strategy will be successful.

Standard & Poor’s 500 (S&P 500) - a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy.

Russell 2000 – The index measures the performance of the small-cap segment of the US equity universe. It is a subset of the Russell 3000 and includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership.

MSCI ACWI ex USA – The index measures the performance of the large and mid-cap segments of the particular regions, excluding USA equity securities, including developed and emerging markets. It is free float-adjusted market-capitalization weighted.

Federal Funds Rate - refers to the target interest rate set by the Federal Open Market Committee (FOMC). This target is the rate at which commercial banks borrow and lend their excess reserves to each other overnight.

This report was prepared by Hobbs Wealth Management, a State registered investment adviser under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Neither the information nor any opinion expressed it so be construed as solicitation to buy or sell a security of personalized investment, tax, or legal advice. For more information please visit: https://adviserinfo.sec.gov/ and search for our firm name.

This newsletter is prepared to provide a degree of insight into the analysis used by Hobbs Wealth Management to make investment decisions. It is not a complete description of all the factors used by Hobbs Wealth Management to make decisions on behalf of clients. The opinions included are not intended to be taken as fact but are Hobbs Wealth Management’s interpretation of the impact of external events on investments.

The information herein was obtained from various sources. Hobbs Wealth Management does not guarantee the accuracy or completeness of information provided by third parties. The information in this report is given as of the date indicated and is believed to be reliable. Hobbs Wealth Management assumes no obligation to update this information, or to advise on further developments relating to it.

This article contains external links directing you to a third-party website. Although we have reviewed the website prior to creating the link, we are not responsible for the content of the site.

An index is an unmanaged portfolio of specific securities, the performance of which is often used as a benchmark in judging the relative performance of certain asset classes. Investors cannot invest directly in an index. An index does not charge management fees or brokerage expenses, and no such fees or expenses were deducted from the performance shown.

The mention of specific securities and sectors illustrates the application of our investment approach only and is not to be considered a recommendation. The specific securities identified and described herein do not represent all of the securities purchased or sold for the portfolio, and it should not be assumed that investment in these securities was or will be profitable. There is no assurance that the securities purchased remain in the portfolio, or that securities sold have not been repurchased. For a complete list of holdings, please contact your portfolio advisor.

Hobbs Wealth Management may discuss and display charts, graphs, formulas, stock and sector picks which are not intended to be used by themselves to determine which securities to buy or sell, or when to buy or sell them. This specific information is limited and should not be used on their own to make investment decisions. This information is offered as educational only.